Imagine you want to buy a flight ticket. You check the price today. It is $300. But you hesitate. What if it drops to $250 tomorrow? So you wait. The next day, the price jumps to $400. Now you regret not buying earlier.

This is called timing the market. And it rarely works.

Investing works the same way. Many beginners freeze because they are afraid of buying at the “wrong” time. What if the price drops right after they invest?

Dollar cost averaging (DCA) solves this problem. Instead of trying to guess the perfect moment, you invest smaller amounts regularly – no matter what the market is doing.

Before you start: If you haven’t already, read our beginner’s guide on how to start investing with $100 or less first. It covers opening your first account and choosing an ETF.

In this guide, I will explain how DCA works, why it reduces stress, and how you can start using it today with as little as $25 per month.

What You Will Learn

- What dollar‑cost averaging actually means

- A real example using the SPY ETF (S&P 500) from Sep 2023 – Feb 2025

- Why trying to time the market can cost you money

- How to start using DCA with any amount

- The one situation where DCA is not the best choice

What Is Dollar Cost Averaging (DCA)?

Dollar cost averaging is an investment strategy where you invest a fixed amount of money at regular intervals – regardless of the asset’s price.

| Key Element | What It Means |

|---|---|

| Fixed amount | You invest the same dollar amount each time (e.g., $100 per month) |

| Regular intervals | You invest on a schedule (e.g., every payday, once per month) |

| Regardless of price | You buy whether the market is up, down, or sideways |

As a result, you automatically buy more shares when prices are low and fewer shares when prices are high. Over time, this lowers your average cost per share.

For example, instead of investing $5,000 once per year, you invest $416 each month. Therefore, you avoid the risk of investing all your money right before a market drop.

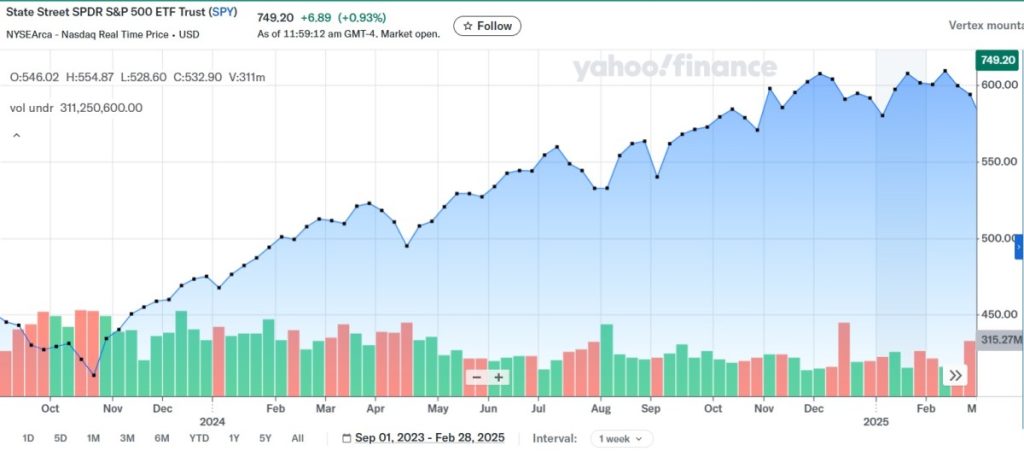

A Real Example: DCA Using the SPY ETF (Sep 2023 – Feb 2025)

Let us look at actual market data. SPY is an ETF that tracks the S&P 500 index. It is one of the most popular ETFs for beginners.

Imagine you decided to invest $500 every month from September 2023 to February 2025 (the last 18 months). Here is what you would have bought, using real monthly prices:

| Month | SPY Price | $500 Buys |

|---|---|---|

| Sep 2023 | $427.48 | 1.17 shares |

| Oct 2023 | $418.20 | 1.20 shares |

| Nov 2023 | $456.40 | 1.10 shares |

| Dec 2023 | $475.31 | 1.05 shares |

| Jan 2024 | $482.88 | 1.04 shares |

| Feb 2024 | $508.08 | 0.98 shares |

| Mar 2024 | $523.07 | 0.96 shares |

| Apr 2024 | $501.98 | 1.00 shares |

| May 2024 | $527.37 | 0.95 shares |

| Jun 2024 | $544.22 | 0.92 shares |

| Jul 2024 | $550.81 | 0.91 shares |

| Aug 2024 | $563.68 | 0.89 shares |

| Sep 2024 | $573.76 | 0.87 shares |

| Oct 2024 | $568.64 | 0.88 shares |

| Nov 2024 | $602.55 | 0.83 shares |

| Dec 2024 | $586.08 | 0.85 shares |

| Jan 2025 | $601.82 | 0.83 shares |

| Feb 2025 | $594.18 | 0.84 shares |

| Total | 17.27 shares |

Total invested: $9,000 (18 months × $500)

Portfolio value in Feb 2025: 17.27 shares × $594.18 = $10,261

Total gain: +$1,261 (a 14% return)

Notice what happened: The market had its ups and downs, but the DCA investor bought more shares when prices were lower (e.g., in Oct 2023 at 418). Consequently, their average cost per share was much lower than the market price at the end of the period. Therefore, they turned a $9,000 investment into $10,261 without any stress of trying to “time” the market.

What If You Tried to Time the Market Badly?

Now let us compare DCA with a realistic poor market‑timing attempt – someone who tries to be smart but ends up losing a small amount of money.

Imagine Alex has $9,000 to invest over the same period (Sep 2023 – Feb 2025). Instead of investing regularly, Alex watches the market and makes these emotional mistakes:

- November 2024 (price 603): The market is at an all−time high. Alex thinks it will keep rising and invests $4,000.

- December 2024 (price 586): The market drops slightly. Alex adds $3,000, thinking it’s a bargain.

- January 2025 (price 602): The market rebounds. Alex puts in the remaining $2,000, afraid of missing out.

Alex’s result:

- Total invested: $9,000

- Shares bought: ($4,000÷603) + ($3,000÷586) + ($2,000÷602) = 6.63 + 5.12 + 3.32 = 15.07 shares

- Value in Feb 2025 ($594.18):15.07 × 594.18 = $8,956

- Loss: -$44 (0.5%)

Now compare that to the disciplined DCA investor over the same period:

| Investor | Method | Total Invested | Final Value | Gain/Loss |

|---|---|---|---|---|

| DCA (disciplined) | $500 monthly | $9,000 | $10,258 | +$1,258 (14%) |

| Alex (bad timer) | Multiple wrong timings | $9,000 | $8,956 | -$44 (0.5%) |

The lesson: With the same $9,000, DCA turned a 14% gain while bad timing led to a small loss. Trying to outsmart the market by buying “on dips” or “at peaks” can backfire. DCA removes the emotional guesswork and keeps you disciplined.

Why DCA Removes the Fear of Timing the Market

Many beginners never start investing because they are waiting for the “right time.”

| Fear | How DCA Helps |

|---|---|

| “What if the market crashes tomorrow?” | You invest small amounts. Therefore, only a small portion is exposed. |

| “I don’t know when to buy.” | You buy on a fixed schedule. No guesswork. |

| “What if I buy at the peak?” | Over time, your average cost smooths out the peaks and valleys. |

| “I am too busy to watch the market.” | DCA is automatic. Set it up once and forget it. |

For example, imagine you started investing $500 per month in 2023 using the SPY example above. The market went up and down. But because you kept buying, you profited from both the dips and the rises.

This is the psychological benefit of DCA. It removes the stress of being “right” and replaces it with the peace of mind that comes from consistency.

How to Start Using Dollar Cost Averaging Today

You can start DCA with any amount, using almost any investment account. We covered how to choose your first ETF and open an account in our investing with $100 guide.

Step 1: Choose Your Investment

For most beginners, a low‑cost ETF (like SPY, VOO, or a global fund like VT) is the best choice. It is diversified and has a strong long‑term track record.

Step 2: Set Your Schedule and Amount

| Schedule | Recommended For |

|---|---|

| Monthly | Most beginners (aligns with payday) |

| Bi‑weekly | If you get paid every two weeks |

| Quarterly | If you prefer larger, less frequent investments |

Start with an amount that feels comfortable. For instance, $25, $50, or $100 per month.

Step 3: Automate It

Most brokers and robo‑advisors allow you to set up automatic transfers and purchases.

What to do:

- Link your bank account to your investment account.

- Set up a recurring transfer of your chosen amount.

- Set up automatic purchase of your chosen ETF (many brokers offer this).

- Then, ignore the short‑term price movements.

As a result, you will invest consistently without ever thinking about it.

When DCA Is Not the Best Choice

Dollar‑cost averaging is excellent for regular investors who are adding money from their paycheck.

However, there is one situation where a lump sum investment has historically performed better.

If you already have a large sum of money (e.g., an inheritance or a bonus), studies show that investing it all at once (lump sum) has outperformed DCA about two‑thirds of the time. Why? Because markets tend to go up over the long term.

But the difference is often small. Therefore, if investing a large lump sum feels emotionally difficult, DCA is still a good choice. Peace of mind matters more than maximizing every single percentage point.

| Situation | Recommended Approach |

|---|---|

| Investing from your monthly salary | DCA (automatic, stress‑free) |

| You have a large lump sum and are emotionally comfortable | Lump sum (historically slightly better returns) |

| You have a large lump sum but feel anxious | DCA over 6–12 months (peace of mind) |

Common Questions About Dollar Cost Averaging

Q: Does DCA guarantee I will not lose money?

No. If the market goes down over a long period, you can still lose value. However, DCA reduces the risk of investing at the absolute worst time.

Q: How often should I invest?

Monthly is the most common and easiest to automate. Align it with your payday.

Q: What if the market is at an all‑time high?

Invest anyway. For example, the market is often at all‑time highs. Over long periods (10+ years), it has always gone higher.

Q: Can I use DCA with cryptocurrencies?

Yes. Many crypto exchanges allow automatic purchases (e.g., $10 of Bitcoin per week). But be aware that crypto is far more volatile than stock ETFs.

Q: Should I invest using DCA if I don’t have an emergency fund yet?

No. First build a small emergency fund (3–6 months of expenses). DCA is for money you can leave invested for 5+ years. Read our guide on building an emergency fund before you start investing.

My Take (Finance Mojito Style)

Dollar‑cost averaging is not about getting the best possible return. It is about getting started and staying consistent.

Here is what I have learned: many people never invest because they are waiting for perfect conditions. They wait for the market to drop. Then they wait for it to drop more. Then they miss the recovery.

DCA removes all of that noise.

You do not need to be smart. You do not need to be lucky. You just need to be consistent.

Set up an automatic $25 or $50 per month into a simple ETF. Do not check the price every day. Do not panic when the market dips. Just keep buying.

Five years from now, you will be glad you started.

Your 30‑Day Action Plan

| Week | Action |

|---|---|

| Week 1 | Choose an ETF (e.g., SPY, VOO, or VT). Read our investing with $100 guide if you need help. |

| Week 2 | Open a brokerage account if you have not already. |

| Week 3 | Set up an automatic monthly transfer of $25–100 from your bank account. |

| Week 4 | Set up automatic purchase of your chosen ETF on the same schedule. |

As a result, one month from today, you will be an automatic, consistent investor – without any stress about timing the market.

Related Guides

Before you start dollar‑cost averaging, make sure you have the basics covered:

- How to Start Investing with $100 or Less – A beginner‑friendly guide to opening your first account and choosing an ETF.

- How to Build a 6‑Month Emergency Fund – Do not invest a single dollar until you have a safety net in place.

Before You Go

Dollar‑cost averaging is one of the simplest and most effective ways to build wealth over time. It removes fear, builds discipline, and works whether you are investing $25 or $2,000 per month.

Next up: How to Store Cryptocurrency Safely (Hot vs Cold Wallets)

Discover more from Finance Mojito

Subscribe to get the latest posts sent to your email.